Recorded: March 11, 2014

Terms of Use: ../info

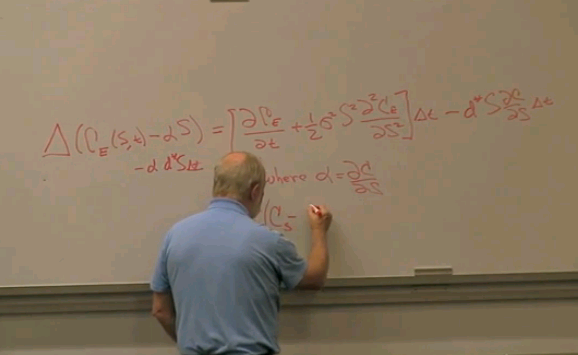

Lecture 15

Course Description: After reviewing tools from probability, statistics, and elementary differential and partial differential equations, concepts such as hedging, arbitrage, Puts, Calls, the design of portfolios, the derivation and solution of the Blac-Scholes, and other equations are discussed.

The notes for this course, Math 176, Mathematics of Finance, have been published as a book:

Saari, Donald G. (2019). Mathematics of Finance: An Intuitive Introduction. Springer.

ISBN-10: 3030254429

ISBN-13: 978-3030254421

This book is copyrighted and is not covered by a Creative Commons license.

Required attribution: Saari, Donald. Math 176 (UCI Open: University of California, Irvine), ../courses/math_176_math_of_finance.html. [Access date]. License: Creative Commons Attribution-ShareAlike 4.0 United States License.